Monitor Your Credit

First Fed makes monitoring your credit easy and free using our Online Banking or mobile app!

Benefits You'll Love

- Check your credit on demand

- See tips for improving your score

- Get alerts when your credit score changes

Monitor your credit score for free using Online Banking or the mobile app!

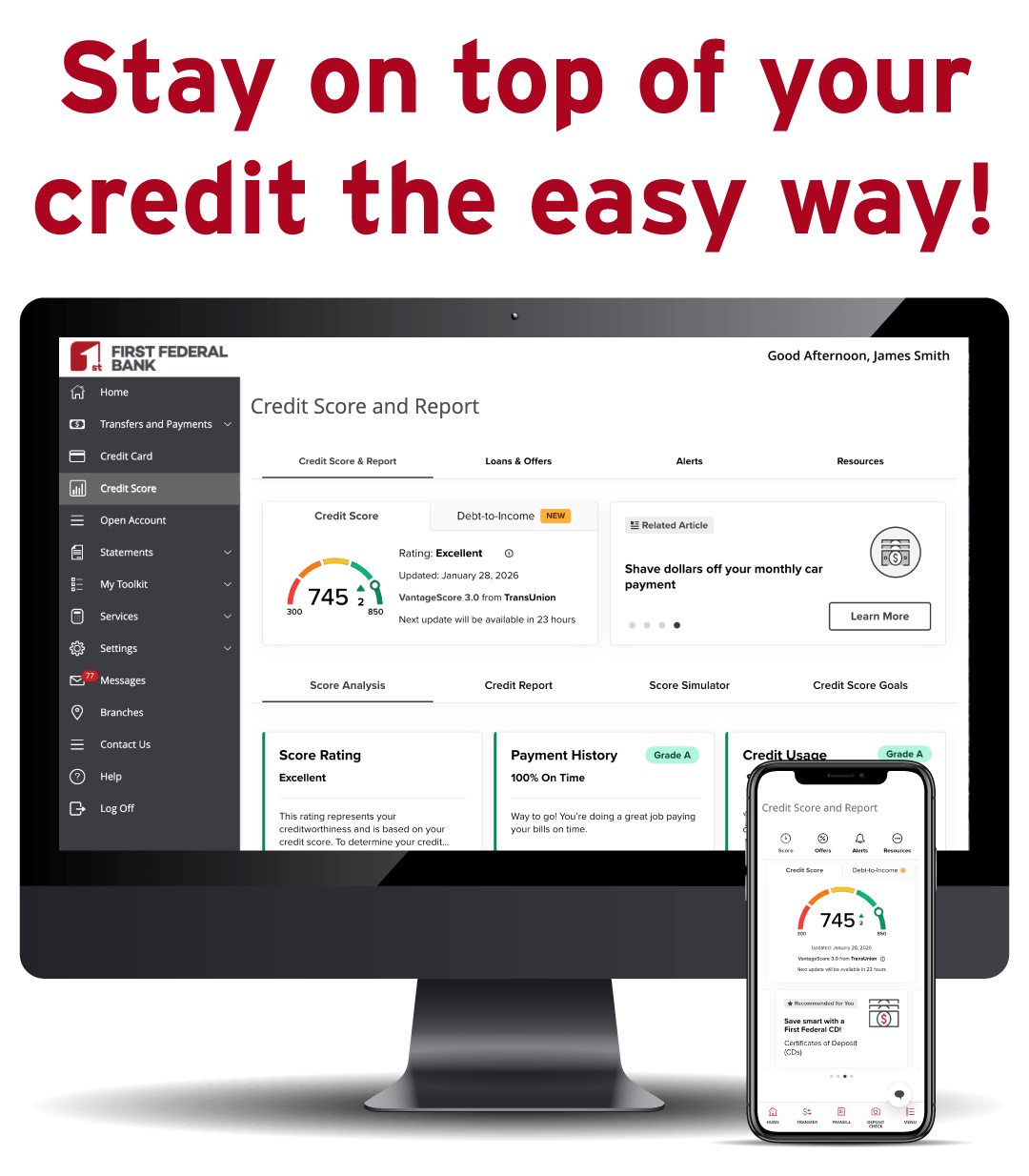

Stay on top of your credit the easy way! Online Banking features a free credit monitoring system that lets you check your credit on demand, see tips for improving your score, and sign up to get alerts when your credit score changes.

If you don't have Online Banking yet, click here to sign up! Once you're enrolled you can see your credit report on your desktop computer or by downloading the FirstFed Mobile App.

You can download the Apple (iOS) version here: Apple App Store

You can download the Android version here: Google Play

*All credit products subject to approval.

{beginAccordion}

What is SavvyMoney Credit Score?

SavvyMoney is a comprehensive Credit Score program offered by First Federal, that helps you stay on top of your credit. You get your latest credit score and report, an understanding of key factors that impact the score, and can see the most up to date offers that can help reduce your interest costs. With this program, you always know where you stand with your credit and how First Federal can help save you money.

Credit Score also monitors your credit report daily and informs you by email if there are any big changes detected such as: a new account being opened, change in address or employment, a delinquency has been reported or an inquiry has been made. Monitoring helps users keep an eye out for identity theft.

What is SavvyMoney Credit Report?

SavvyMoney Credit Report provides you all the information you would find on your credit file including a list of open loans, accounts and credit inquiries. You will also be able to see details on your payment history, credit utilization and public records that show up on your account. Like Credit Score, when you check your credit report, there will be no impact to your score.

Is there a fee?

No. SavvyMoney is entirely free and no credit card information is required to register.

How often is my credit score updated?

As long as you are a regular online banking user, your credit score will be updated every month and displayed in your online banking screen. You can click “refresh score” as frequently as every day by navigating to the detailed SavvyMoney site from within online banking.

How does the SavvyMoney Credit Score differ from other credit scoring offerings?

SavvyMoney pulls your credit profile from TransUnion, one of the three major credit reporting bureaus, and uses VantageScore 3.0, a credit scoring model developed collaboratively by the three major credit bureaus: Equifax, Experian, and TransUnion. This model seeks to make score information more uniform between the three bureaus to provide consumers a better picture of their credit health.

Why do credit scores differ?

There are three major credit-reporting bureaus—Equifax, Experian and Transunion—and two scoring models—FICO or VantageScore—that determine credit scores. Financial institutions use different bureaus, as well as their own scoring models. Over 200 factors of a credit report may be taken into account when calculating a score and each model may weigh credit factors differently, so no scoring model is completely identical. No matter what credit bureau or credit scoring model is used, consumers do fall into specific credit ranges: Excellent 781–850, Good 661-780, Fair 601-660, Unfavorable 501-600, Bad Below 500.

Will First Federal use SavvyMoney Credit Score to make loan decisions?

No, First Federal uses its own lending criteria for making loan decisions.

Will SavvyMoney share my credit score with First Federal?

SavvyMoney Credit Score is a free service to help users understand their credit health, make improvements in their scores, and see loan and credit card offers from First Federal. First Fed doesn’t have access to users’ credit files with SavvyMoney unless the users choose to share them. If they would like to share, they can easily do so by navigating to the Credit Report tab and clicking “Download Report” to share at their discretion.

How does SavvyMoney Credit Score keep my financial information secure?

SavvyMoney uses bank level encryption and security measures to keep your data safe and secure. Your personal information is never shared with or sold to a third party.

If First Federal doesn’t use SavvyMoney Credit Score to make loan decisions, why do we offer it?

SavvyMoney Credit Score can help you manage your credit so when it comes time to borrow for a big-ticket purchase—like buying a home, car or paying for college—you have a clear picture of your credit health and can qualify for the lowest possible interest rate. You’ll also see offers on how you can save money on your new and existing loans with First Federal.

What if the information provided by SavvyMoney Credit Score appears to be wrong or inaccurate?

The SavvyMoney Credit Score makes its best effort to show you the most relevant information from your credit report. If you think that some of the information is wrong or inaccurate, we encourage you to take advantage of obtaining free credit reports from www.annualcreditreport.com, and then pursuing with each bureau individually. Each bureau has its own process for correcting inaccurate information but every user can “File a Dispute” by clicking on the “Dispute” link within their SavvyMoney Credit Report. However, The Federal Trade Commission website offers step-by-step instructions on how to contact the bureaus and correct errors.

Will accessing SavvyMoney Credit Score ‘ping’ my credit and potentially lower my credit score?

No. Checking SavvyMoney Credit Score is a “soft inquiry”, which does not affect your credit score. Lenders use ‘hard inquiries’ to make decisions about your credit worthiness when you apply for loans.

Does SavvyMoney offer credit report monitoring as well?

Yes. SavvyMoney will monitor and send email alerts when there’s been a change to your credit profile.

How do I change my email address or other personal information?

There are three ways to update contact information - such as phone number, email, and mailing address:

- Call the Customer Service Center

- Send a Secure Message in Online Banking

- In-person at a Branch

Can people use SavvyMoney on mobile devices?

Yes, SavvyMoney Credit Score is available for both mobile and tablet devices and is integrated inside our mobile application.

{endAccordion}

Use this calculator to determine your projected earnings from our Kasasa Cash account. Move the sliders or type in the numbers to see your potential rewards.

- Estimated Annual Rewards $0

- Estimated monthly interest earned* $0

- Monthly ATM fees refunded**$0

This calculator compares the costs of buying or leasing a vehicle. There are three sections to complete, and you can adjust and experiment with different scenarios.

- Net cost of buying $0

- Net cost of leasing $0

A fixed-rate, fixed-term CD can earn higher returns than a standard savings account. Use this calculator to get an estimate of your earnings. Move the sliders or type in numbers to get started.

- Total value at maturity $0

- Total interest earned $0

- Annual Percentage Yield (APY)0.000%

Whether it's a down payment, college, a dream vacation...a savings plan can help you reach your goal. Use the sliders to experiment based on length of time and amount per month.

- Monthly deposit needed to reach goal $0

This calculator can help you get a general idea of monthly payments to expect for a simple loan. Move the sliders or type in numbers to get started.

- Estimated monthly payment $0

- Total paid $0

- Total interest paid $0

Business Money Market

| Tier | Average Daily Balance Range | Interest Rate | Annual Percentage Yield (APY) |

|---|---|---|---|

| 1 | Below $1,000.00 | 0.0500% | 0.05% |

| 2 | Equal to or greater than $1,000.00 but less than $10,000.00 | 0.2000% | 0.20% |

| 3 | Equal to or greater than $10,000.00 but less than $25,000.00 | 0.4000% | 0.40% |

| 4 | Equal to or greater than $25,000.00 but less than $50,000.00 | 0.6500% | 0.65% |

| 5 | Equal to or greater than $50,000.00 but less than $100,000.00 | 0.8500% | 0.85% |

| 6 | Equal to or greater than $100,000.00 but less than $250,000.00 | 1.1000% | 1.11% |

| 7 | Equal to or greater than $250,000.00 but less than $500,000.00 | 1.6000% | 1.61% |

| 8 | Equal to or greater than $500,000.00 but less than $1,000,000.00 | 2.1000% | 2.12% |

| 9 | Equal to or greater than $1,000,000.00 but less than $2,500,000.00 | 2.6000% | 2.63% |

| 10 | Equal to or greater than $2,500,000.00 | 3.0000% | 3.04% |

Rates are accurate as of 6/24/2026. Your interest rate and annual percentage yield may change. At our discretion, we may change the interest rate on your account. We may change the interest rate on your account at any time. There are no maximum or minimum interest rate limits for this account. Interest will be compounded monthly and will be credited to the account monthly. If you close your account before interest is credited, you will receive the accrued interest. You must deposit $1,000.00 to open this account. A service fee of $10.00 will be imposed every month if the average daily balance for the month falls below $1,000.00. You must maintain a minimum average daily balance of $5.00 to obtain the disclosed annual percentage yield. A dormant account fee of $5.00 per month will be charged after 12 months of inactivity. Interest earnings credited to the account, if any, are not considered account activity.

We use the average daily balance method to calculate interest on your account. This method applies a periodic rate to the average daily balance in the account for the period. The average daily balance is calculated by adding the principal in the account for each day of the period and dividing that figure by the number of days in the period. The average daily balance that we use when calculating interest is the collected balance. That means we only include those funds for which we have actually received payment when we determine the average daily balance on which interest is paid. Interest begins to accrue no later than the business day we receive credit for the deposit of noncash items (for example, checks). Withdrawals from your MMDA are limited to six (6) per statement cycle. A fee of $10.00 will be charged for each transaction in excess of limit. Please refer to the separate Fee Schedule provided to you with this disclosure for information about fees and charges associated with this account. A Fee Schedule will be provided to you at the time you open an account, periodically when fees or charges change, and upon request.

Certificates of Deposit (CDs)

| Term | Interest Rate | APY |

|---|---|---|

| 5-Month Rate w/ Checking1 | 3.50% | 3.56% |

| 5-Month Rate w/o Checking1 | 2.91% | 2.95% |

| 3 Months | 3.45% | 3.51% |

| 6 Months | 3.30% | 3.35% |

| 12 Months | 3.25% | 3.30% |

| 18 Months | 3.15% | 3.20% |

| 30 Months | 3.20% | 3.25% |

| 4 Years | 3.30% | 3.35% |

| 5 Years | 3.35% | 3.40% |

$500 Minimum Deposit to Open.

Interest rates and APYs are accurate as of 1/1/2026. Rates are subject to change at any time.

Annual Percentage Yield (APY) assumes interest credited is not withdrawn until maturity or renewal. Principal withdrawals prior to the maturity or renewal date may be subject to early withdrawal penalties. Penalties are not assessed if the account holder is deceased. Renewal grace period is seven (7) calendar days. Fees may reduce earnings on the account.

1Customers with a new or existing First Federal checking account earn 3.50% with an annual percentage yield (APY) of 3.56%. This APY is accurate as of 6/24/2026. This offering is for a limited time and subject to change at any time. Interest will be compounded and credited monthly. The APY assumes there are no withdrawals until maturity or renewal. Customers without a First Federal checking account earn 2.91% with an annual percentage yield (APY) of 2.95%. All other terms and conditions referenced above (*) apply.

Home Equity Loans

Rates and APRs below as of 07/17/2026.

| Product | Rate | APR |

|---|---|---|

| Home Equity Line of Credit (HELOC)1 | 6.500% | 6.500% |

| Home Equity Loan2 | 6.250% | 6.284% |

For products not listed above, including government insured, please call (208) 733-4222.

1HELOC stated Annual Percentage Rate (APR) subject to criteria, including automatic payment from a First Federal checking account. HELOC initial payment is interest-only. Line of credit is accessible for ten years followed by a fifteen-year repayment period. Variable interest rate may increase after consummation. Property insurance may apply. Maximum APR of 18.00%. Borrower may be responsible for third-party costs that may range from $250 to $5,000. Borrower is responsible for appraisal fees on loans exceeding $400,000. In Idaho, the title insurance premium (if applicable) and mortgage recording tax will be based on the maximum amount of the credit line available to you, regardless of how much is advanced to you at any time. Rate quoted is for liens in first position. Loans in second lien position will have higher rates.

2Rates vary by qualification and term selected. Rate quoted is for liens in first position. Loans in second lien position will have higher rates.

Jumbo Certificates of Deposit

| Term | Interest Rate | APY |

|---|---|---|

| 5 - Month Rate w/ Checking1 | 3.60% | 3.66% |

| 5 - Month Rate w/o Checking1 | 3.01% | 3.05% |

| 3 Months | 3.55% | 3.61% |

| 6 Months | 3.40% | 3.45% |

| 12 Months | 3.35% | 3.40% |

| 18 Months | 3.25% | 3.30% |

| 30 Months | 3.30% | 3.35% |

| 4 Years | 3.40% | 3.45% |

| 5 Years | 3.45% | 3.51% |

$100,000 minimum deposit to open.

Interest rates and APYs are accurate as of 6/24/2026 Rates are subject to change at any time.

Annual Percentage Yield (APY) assumes interest credited is not withdrawn until maturity or renewal. Principal withdrawals prior to the maturity or renewal date may be subject to early withdrawal penalties. Penalties are not assessed if the account holder is deceased. Renewal grace period is seven (7) calendar days. No minimum balance is required to obtain the disclosed APY. Fees may reduce earnings on the account.

1 Customers with a new or existing First Federal checking account earn 3.60% with an annual percentage yield (APY) of 3.66%. This APY is accurate as of 6/24/2026. This offering is for a limited time and subject to change at any time. Interest will be compounded and credited monthly. The APY assumes there are no withdrawals until maturity or renewal. Customers without a First Federal checking account earn 3.01% with an annual percentage yield (APY) of 3.05%. All other terms and conditions referenced above (*) apply.

Kasasa Cash*

| Balance | Minimum Opening Deposit | Rate | APY |

|---|---|---|---|

| 0 - $15,000 | $x | 0.00% | 0.00% |

| $15,000+ | $x | 0.00% | 0.00% |

| All balances if qualifications not met | $x | 0.00% | 0.00% |

Qualifications

xx

Kasasa Saver*

| Balance | Minimum Opening Deposit | Rate | APY |

|---|---|---|---|

| 0 - $15,000 | $x | 0.00% | 0.00% |

| $15,000+ | $x | 0.00% | 0.00% |

| All balances if qualifications not met | $x | 0.00% | 0.00% |

Qualifications

xx

Loan Rates

Loan Rates

Money Market

| Tier | Average Daily Balance Range | Interest Rate | Annual Percentage Yield (APY) |

|---|---|---|---|

| 1 | Below $1,000.00 | 0.0500% | 0.05% |

| 2 | Equal to or greater than $1,000.00 but less than $10,000.00 | 0.2000% | 0.20% |

| 3 | Equal to or greater than $10,000.00 but less than $25,000.00 | 0.4000% | 0.40% |

| 4 | Equal to or greater than $25,000.00 but less than $50,000.00 | 0.6500% | 0.65% |

| 5 | Equal to or greater than $50,000.00 but less than $100,000.00 | 0.8500% | 0.85% |

| 6 | Equal to or greater than $100,000.00 but less than $250,000.00 | 1.1000% | 1.11% |

| 7 | Equal to or greater than $250,000.00 but less than $500,000.00 | 1.6000% | 1.61% |

| 8 | Equal to or greater than $500,000.00 but less than $1,000,000.00 | 2.1000% | 2.12% |

| 9 | Equal to or greater than $1,000,000.00 but less than $2,500,000.00 | 2.6000% | 2.63% |

| 10 | Equal to or greater than $2,500,000.00 | 3.0000% | 3.04% |

Rates are accurate as of 6/24/2026. Your interest rate and annual percentage yield may change. At our discretion, we may change the interest rate on your account. We may change the interest rate on your account at any time. There are no maximum or minimum interest rate limits for this account. Interest will be compounded monthly and will be credited to the account monthly. If you close your account before interest is credited, you will receive the accrued interest. You must deposit $1,000.00 to open this account. A service fee of $10.00 will be imposed every month if the average daily balance for the month falls below $1,000.00. You must maintain a minimum average daily balance of $5.00 to obtain the disclosed annual percentage yield. A dormant account fee of $5.00 per month will be charged after 12 months of inactivity. Interest earnings credited to the account, if any, are not considered account activity.

We use the average daily balance method to calculate interest on your account. This method applies a periodic rate to the average daily balance in the account for the period. The average daily balance is calculated by adding the principal in the account for each day of the period and dividing that figure by the number of days in the period. The average daily balance that we use when calculating interest is the collected balance. That means we only include those funds for which we have actually received payment when we determine the average daily balance on which interest is paid. Interest begins to accrue no later than the business day we receive credit for the deposit of noncash items (for example, checks). Withdrawals from your MMDA are limited to six (6) per statement cycle. A fee of $10.00 will be charged for each transaction in excess of limit. Please refer to the separate Fee Schedule provided to you with this disclosure for information about fees and charges associated with this account. A Fee Schedule will be provided to you at the time you open an account, periodically when fees or charges change, and upon request.

SuperSaver Savings

| Daily Balance Range | Interest Rate | Depending on Account Balance, Annual Percentage Yield (APY1) will: |

|---|---|---|

| $0.01 to $500.00 | 10.00% | Equal 10.47% APY |

| NEXT $500 $500.01 to $1,000.00 |

5.00% | Range from 10.47% to 7.79% APY |

| NEXT $1,000 $1,000.01 to $2,000.00 |

1.00% | Range from 7.79% to 4.40% APY |

| Greater than $2,000.00 | 0.10% | Range from 4.40% to 0.10% APY |

1 To qualify for the Annual Percentage Yield (APY), the following requirements must be met during a monthly statement cycle: Minimum of one (1) Round-Up transfer2 from checking account; minimum of one (1) deposit of at least $30 or two (2) deposits of at least $15; no withdrawal transactions; receive e-statements. If eligibility requirements are not met, the interest rate will be 0.10% with an APY of 0.10%. Interest is compounded and credited monthly. $10 minimum opening deposit required. The APY is accurate as of 6/24/2026. The interest rate on this variable rate account may change at any time at our discretion. Each primary account holder is allowed one (1) SuperSaver account per tax identification number.

2 Round-Up transfers must be posted, not pending or processing.

Vehicle Rates

Rates and APRs below as of 07/02/2026.

| Loan Term | Rate | APR* |

|---|---|---|

| 48-Month | 5.576% | 5.863% |

| 60-Month | 5.576% | 5.807% |

| 72-Month | 5.576% | 5.770% |

Examples loan terms assume:

FICO score >=720 | LTV < 95% | Age of Vehicle <= 6yr (2020 or newer model yr) | *Stated APR subject to criteria, including having an active First Federal Personal Checking Acct at time of closing. Rates, terms and fees subject to approved credit. Valid as of 06/15/2026.